Preprint in Mathematical Finance from our research team

About

The Stochastic Numerics Group would like to highlight the recent achievement within our research group. On the 30th of April, “Data-Driven Stochastic Optimal Control for Intraday Electricity Trading by Renewable Producers” was published on arXiv. The authors of this paper are Assistant Professor Chiheb Ben Hammouda of Utrecht University, PhD student Michael Samet of RWTH, and PI Raul Tempone. We would like to congratulate these authors on the preprint of their paper.

Our research develops a data-driven continuous-time stochastic optimal control framework for intraday electricity trading by renewable energy producers. The work addresses the practical challenge renewable energy producers face due to uncertain production, volatile intraday prices, and imbalance charges when committed sales deviate from actual generation. Renewable production and intraday prices are modeled via data-driven stochastic differential equations, with production following a Jacobi-type diffusion and prices following an asymmetric jump-diffusion model.

A central feature of the framework is its realistic market structure, explicitly incorporating gate closure, the lead time before physical delivery, and imbalance penalties based on cumulative delivered energy over the imbalance settlement period. This leads to a three-stage dynamic programming formulation involving two linear Kolmogorov backward equations and a nonlinear Hamilton-Jacobi-Bellman partial integro-differential equation. To solve the resulting problem, we develop a monotone IMEX finite-difference scheme with operator splitting, semi-implicit treatment of the nonlinear Hamiltonian, and a structure-exploiting differential formulation of the jump operator.

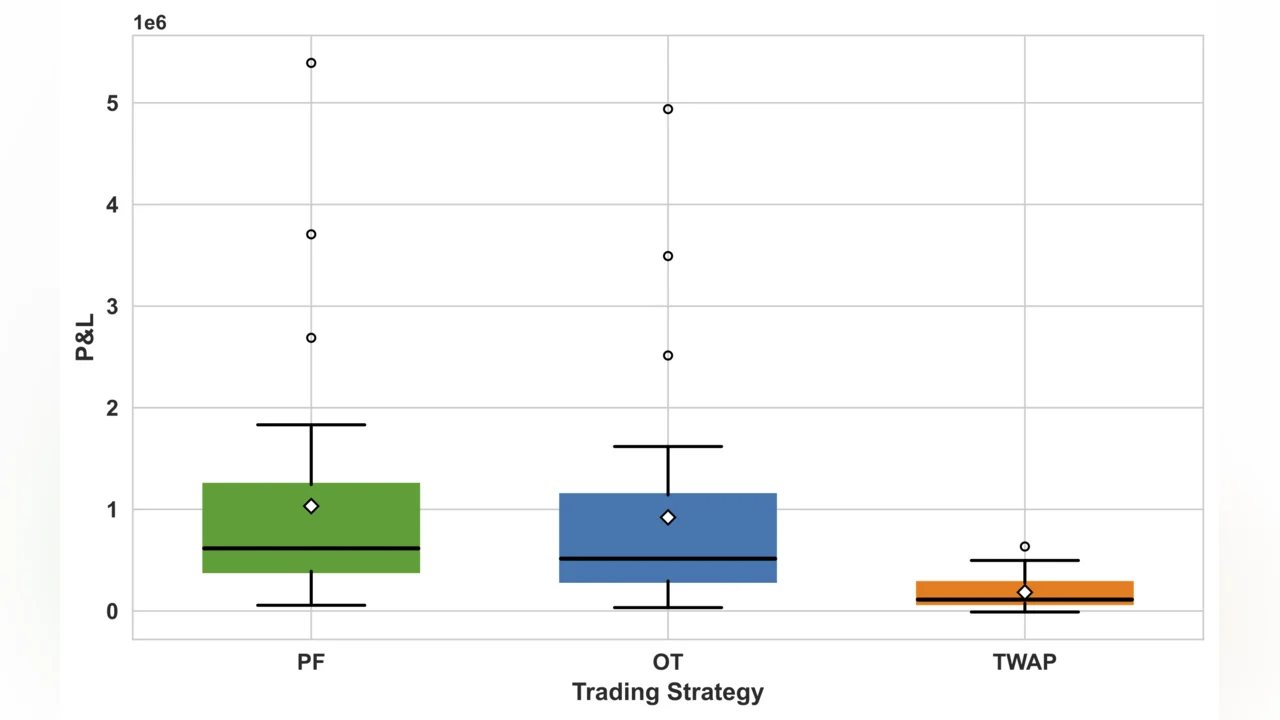

Numerical experiments based on German electricity market data demonstrate that the optimal trading strategy enhances profit-and-loss (P&L) performance compared to a time-weighted average price (TWAP) benchmark and approaches the performance of a perfect-foresight strategy. The study also demonstrates how jump intensity, delivery-window length, liquidity costs, and imbalance penalties impact the optimal trading policy and the resulting profit-and-loss (P&L) profile.

For those interested in learning more about this work, the preprint is available here.

We are excited about the potential impact of our findings and look forward to further exploring and expanding upon this research. Stay tuned for more updates from our team!

ABSTRACT:

The rapid growth of weather-dependent renewable generation increases price volatility and imbalance penalty risk in power markets, creating the need for advanced quantitative trading strategies. We develop a data-driven continuous-time stochastic optimal control framework for intraday electricity trading using stochastic differential equations with drift terms ensuring mean reversion to deterministic forecast trajectories. Production follows a Jacobi diffusion, while prices follow an asymmetric jump-diffusion to reflect the heavy-tailed behavior observed in intraday markets. The framework accounts for realistic market features by incorporating gate closure and energy-based imbalance settlement over the delivery window, where the path-dependent imbalance cost is handled by state augmentation to preserve the Markovian structure. The value function is characterized via the dynamic programming principle by a three-stage sequence of two linear Kolmogorov backward equations and a nonlinear Hamilton-Jacobi-Bellman partial integro-differential equation. To solve this problem efficiently, we propose a monotone IMEX finite-difference scheme with operator splitting, semi-implicit linearization, and a differential formulation for the jump operator. Numerical experiments based on German market data indicate that, under the provided forecasts, the computed strategy outperforms the TWAP benchmark and approaches the perfect-foresight benchmark. Sensitivity experiments further show how jump intensity, delivery-window length, and trading horizon affect the trading policy and the resulting profit-and-loss distribution.