Preprint in numerical analysis by our research team

About

The Stochastic Numerics group is proud to announce the preprint of our research team's paper, “Quasi-Monte Carlo with a Hankel random digital net”, in arXiv. This paper is a culmination of the collaborative work between KAUST postdoctoral fellow, Yang Liu, PI Raul Tempone, and Associate Professor Takashi Goda of the University of Tokyo.

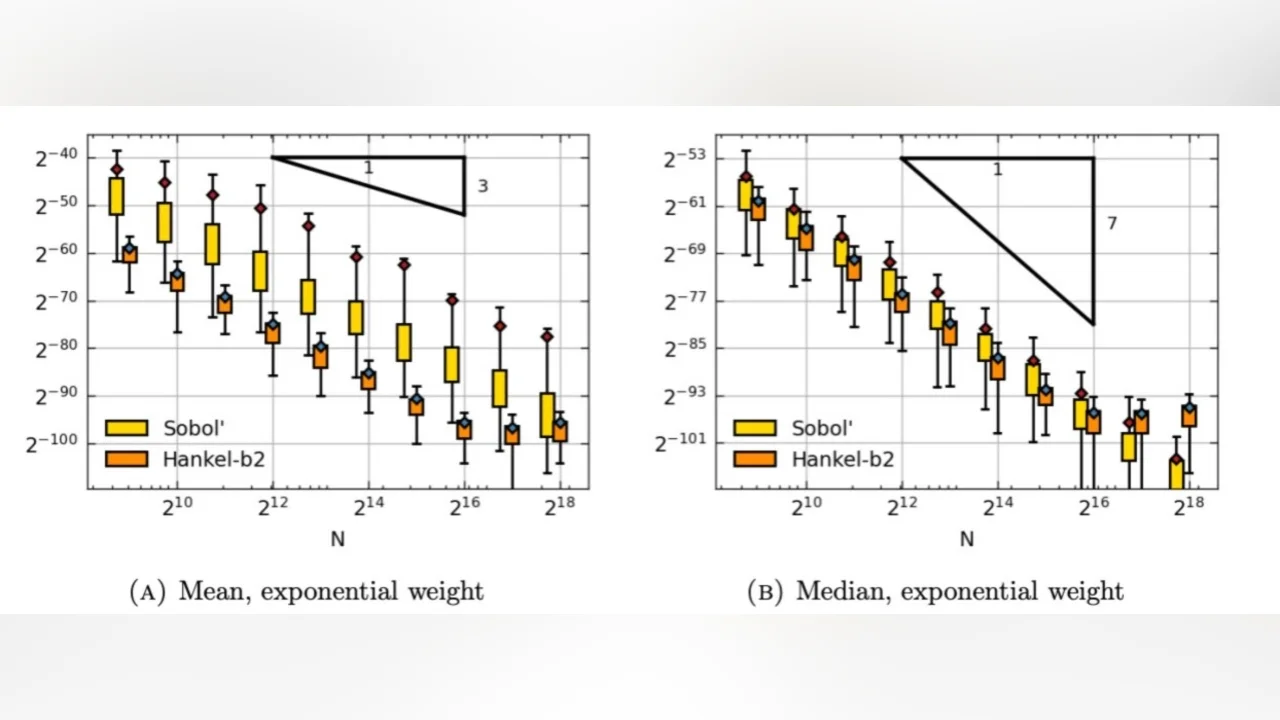

Our research presents a novel randomized quasi-Monte Carlo framework for high-dimensional numerical integration, which is fundamental in applications such as uncertainty quantification, computational finance, and scientific computing. By introducing Hankel random digital nets, we provide a new structured randomization technique that reduces the amount of randomness required while preserving strong theoretical convergence guarantees and improving the practical performance and stability of quasi-Monte Carlo estimators.

For those interested in learning more about this work, the preprint is available here.

We are excited about the potential impact of our findings and look forward to further exploring and expanding upon this research. Stay tuned for more updates from our team!

ABSTRACT:

This paper proposes a new randomized design of digital nets in which the generating matrices are chosen to be random Hankel matrices. Compared with previous randomized designs of digital nets, this approach simplifies the construction process and reduces the number of random variables required, while still achieving desirable convergence rates when combined with appropriate estimators. We analyze the properties of the proposed design, derive bounds for Walsh coefficients, and provide error analysis for both the median-of-means estimator and a newly proposed greedy selection estimator, i.e. the selection of the best design from a batch in terms of a worst-case error bound. Numerical experiments validate our theoretical findings and demonstrate the practical performance of the proposed methods.

Related People

Related Researchers

Yang Liu

- Postdoctoral Research Fellow, Applied Mathematics and Computational Science